I have searched for very profitable companies that pay rich dividends and have a low payout ratio. This kind of stock offers limited downside and provides a very nice income.

I have elaborated a screening method, which shows stock candidates following these lines. Nonetheless, the screening method should only serve as a basis for further research.

The screen's formula requires all stocks to comply with all of the following criteria:

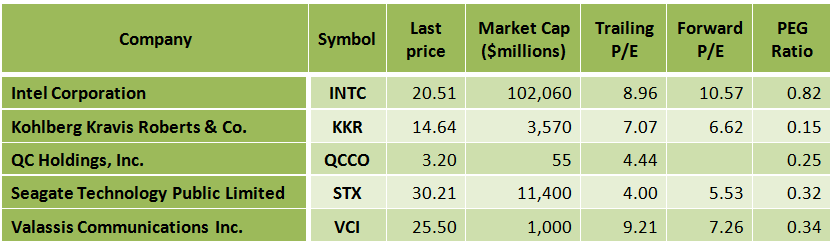

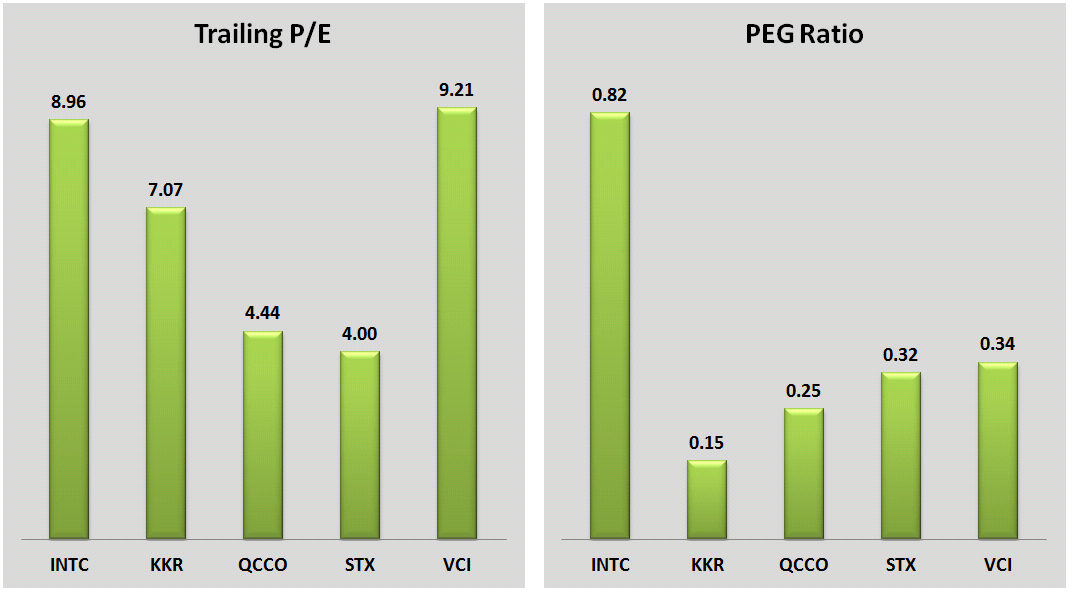

1. Trailing P/E is less than 10.

2. The PEG Ratio is less than 1.00.

3. Price to free cash flow is positive.

4. Average annual earnings growth estimates for the next five years is greater than 10%.

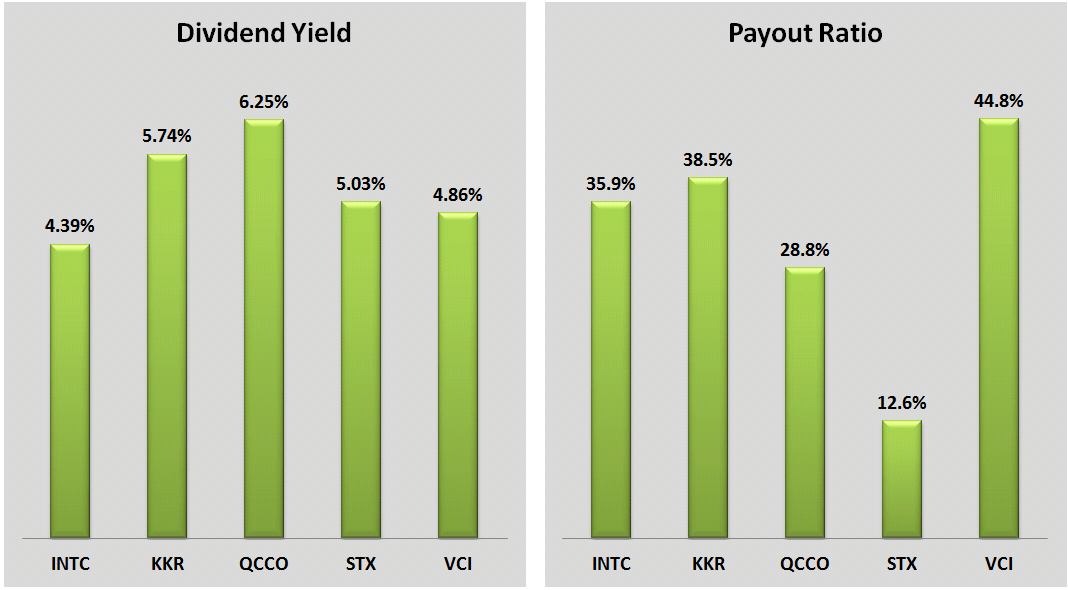

5. Dividend yield is greater than 4.0%.

6. The payout ratio is less than 45%.

After running this screen on December 28, 2012, before the market open, I obtained as results the five following stocks:

(click images to enlarge)

Intel Corporation (INTC)

Intel Corporation designs, manufactures, and sells integrated digital technology platforms primarily in the Asia-Pacific, the Americas, Europe, and Japan.

Intel has a very low debt (total debt to equity is only 0.15), and the trailing P/E is very low at 8.96. The forward P/E is also very at 10.57. The PEG ratio is very low at 0.82, and the average annual earnings growth estimates for the next five years is 10.87%. The forward annual dividend yield is very high at 4.39%, and the payout ratio is only 35.9%. On December 11, Intel launched a data-center chip using low-power technology found in smartphones, stepping up competition in the nascent microserver market and winning a nod from Facebook (here). The Atom chip rolled out on earlier this month uses much less electricity than Intel's previous processors for servers, and comes as Intel's rivals also eye the low-power server niche. Energy-sipping chips similar to those used in smartphones and tablets lack the horsepower of traditional server processors made by Intel. But data centers that combine many low-power chips instead of just a few heavy-duty processors may provide more computing power for less money, and use less electricity. Intel is no longer the fast-growing company it used to be, but with such a low P/E and such a high dividend yield, INTC stock is a safe bet.

Chart: finviz.com

Kohlberg Kravis Roberts & Co. (KKR)

Kohlberg Kravis Roberts & Co. is a private equity investment firm specializing in acquisitions, leveraged buyouts, management buyouts, special situations, growth equity, mature, and middle market investments.

Kohlberg Kravis Roberts has a very low trailing P/E of 7.07, and even a lower forward P/E of 6.62. The PEG ratio is extremely low at 0.15. The price to free cash flow for the trailing 12 months is very low at 1.03. The average annual earnings growth for the past five years was very high at 21.91%, and the average annual earnings growth estimates for the next five years is even much higher at 46.50%. The forward annual dividend yield is very high at 5.74%, and the payout ratio is only 38.5%. Analysts recommend the stock (here) -- among the 13 analysts covering the stock, four rate it as a strong buy, six rate it as a buy and three rate it as a hold. The company is trading 5.24% below its 52-week high, and has 25.9% upside potential based on the consensus mean target price of $18.43. The stock price is 3.85% above its 20-day simple moving average, 1.92% above its 50-day simple moving average and 7.49% above its 200-day simple moving average, which indicates short-term, mid-term and long-term uptrend. On October 26, Kohlberg Kravis Roberts reported its 3Q financial results (here). On that occasion, Henry R. Kravis and George R. Roberts, Co-Chairmen and Co-Chief Executive Officers of KKR, said:

We are pleased with the firm's performance for the nine months through September 30. Our private equity funds appreciated by 20% and our balance sheet investments appreciated by 22%, outperforming the MSCI World Index by over 600 and 800 basis points, respectively.

All these factors -- the very low multiples, the strong growth prospects, the analysts' recommendation, the fact that the stock is in an uptrend and the rich dividend -- make KKR stock quite attractive.

Chart: finviz.com

QC Holdings, Inc. (QCCO)

QC Holdings, Inc. and its subsidiaries provide various retail consumer financial products and services in the United States.

QC Holdings has a low debt (total debt to equity is only 0.48), and it has a very low trailing P/E of 4.44. The PEG ratio is extremely low at 0.25. The price to free cash flow for the trailing 12 months is very low at 7.92, and the average annual earnings growth estimates for the next five years is quite high at 18%. The company is trading 33.15% below its 52-week high, and has 56% upside potential based on the consensus mean target price of $5.00. On November 9, QC Holdings reported its 3Q financial results (here). QCCO reported income from continuing operations of $2.0 million and revenues of $48.8 million for the quarter ended September 30, 2012. For the nine months ended September 30, 2012, income from continuing operations totaled $9.2 million and revenues were $138.3 million. The cheap valuation, strong growth prospects and the fact that QCCO stock is selling way below its book value (price to book value is only 0.64) make QCCO stock quite attractive.

Chart: finviz.com

Seagate Technology Public Limited Company (STX)

Seagate Technology designs, manufactures, markets, and sells hard disk drives for enterprise storage, client compute, and client non-compute market applications worldwide.

Seagate has an extremely low trailing P/E of 4.00, and an extremely low forward P/E of 5.53. The PEG ratio is also very low at 0.32. The price to free cash flow for the trailing 12 months is very low at 3.64, and the price to sales is also very low at 0.72. The average annual earnings growth for the past five years has been very high at 33.07%, and the average annual earnings growth estimates for the next five years is 12.50%. The forward annual dividend yield is very high at 5.03%, and the payout ratio is very low at 12.6%. The stock price is 8.06% above its 20-day simple moving average, 9.43% above its 50-day simple moving average and 9.42% above its 200-day simple moving average.

On October 31, Seagate reported its fiscal first quarter 2013 financial results (here), which were below estimates and the Non-GAAP gross margin was 29%, about a point below guidance. In the quarter, Seagate bought back 20.5 million shares for about $669 million. Although the results were disappointing, I think that a company that has 42% of the world's disk drives market share (here) and is selling with such low multiples is a good investment.

... Continue to read.

No comments:

Post a Comment