|

| English: Stocks Approach - York Road (Photo credit: Wikipedia) |

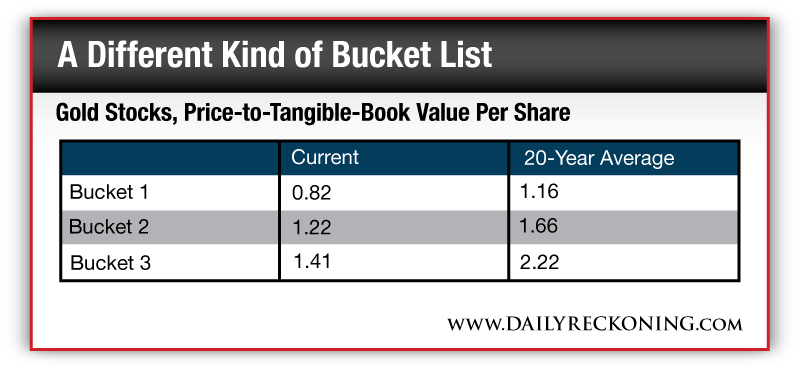

| New York, Jun.23, stock picks .- In an email to my Capital & Crisis readers on March 22, I shared a great speech by Dean Williams, then a senior vice president at Batterymarch Financial. (Delivered in 1981, it was called Trying Too Hard.) The speech was full of great advice, including the following: "There are two ways we can try to gain an edge over the market. The one most of us choose is to try to generate superior information, to know more than anyone else. The other choice is to be better at measuring value than others and not to care very much about what other investors think they know. To hold cheaper securities by today's standards and let the future speak for itself." My path is the latter. Of course, this begs the question: What's objectively cheap by today's standards? I have a few answers. Gold stocks are cheap. One way to see this fact comes from John Doody, editor of The Gold Stock Analyst. Doody compares the price of gold per ounce in the average gold stock as a percentage of the gold price. (Technically, he compares the market cap per ounce of proven and probable reserves against the gold price.) It yields a, shall we say, highly suggestive result. Doody finds that gold stocks currently trade for just 13% of the current price of gold. Put another way, you can buy an ounce of gold by owning a gold stock and pay just $207 an ounce. From 2002-07, the market valued the gold of gold stocks at 38% of the price of gold. Ever since 2007, the percentage has been dropping. And it currently sits at just 13% -- the lowest since at least 2001. As Doody notes, to get to 38% from here, gold stocks would have to triple. We own a pair of gold stocks, both down. Doody, a masterful gold stock picker with a track record better than anyone I know of in this sector, has a portfolio full of losers. It's a tough time for gold stock investors, which is a sign in itself. Bank stocks are also cheap. One way to see their low valuations is to look at price-to-tangible book value per share. I'm not saying price to book holds all the answers. But it is a pretty good, objective proxy for cheapness, much like Doody's percentage measure on gold stocks. It's also wonderfully simple. Let's break down banks into three buckets by asset size. Those with less than $1 billion in assets go in bucket one. Those with $1-10 billion in assets go in bucket two. And bucket three is for the banks with assets above $10 billion. The median multiples for each bucket compared with its 20-year average look like this:  Put another way, these stocks trade for 71%, 74% and 64%, respectively, of their long-term averages. Skeptics would say there are good reasons why bank stocks are cheap. Look at earnings, they'd say. Median price-earnings ratios are around 95% of the 20-year average. "Yes, but," says I "profits move in cycles. They will rebound." When it happens is anybody's guess. As an investor, you focus on what you know today. And what we know today is bank multiples sit well below their 20-year averages. |

||

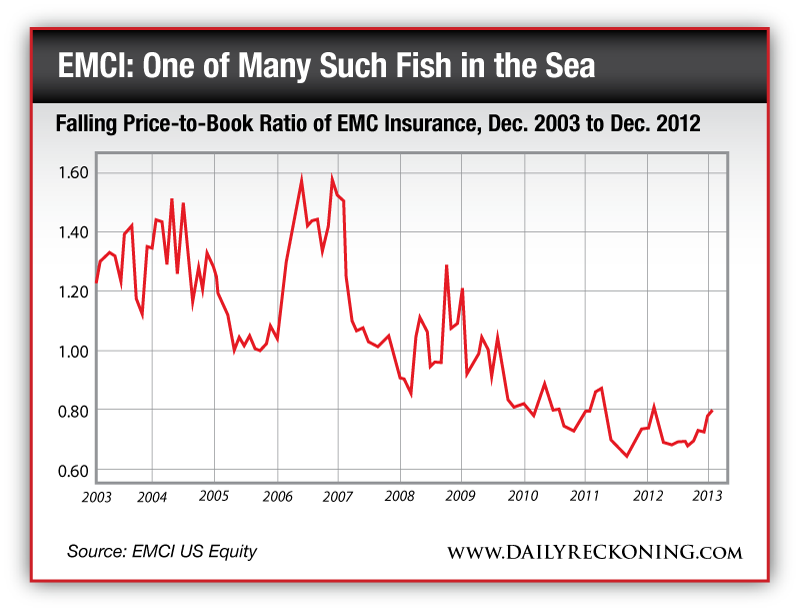

| According to Jeff Davis: "Historically, when bank multiples rose above the 20-year average, returns tended to be poor over the ensuing one- to two-year period and vice versa." We're in the "vice versa" scenario now. Davis, by the way, is the managing director of Mercer Capital's financial institutions group. He writes a good blog for SNL Financial. Mercer has spent "30 years studying equity market returns" and what goes into the mixing bowl that makes them. I got my figures above from him. Importantly, bank acquisitions are still going off at 1.2 times book and greater. These takeovers make tremendous sense, as the buyer can lower costs and improve the economics of the bank. Larger banks, too, enjoy better valuations. The odds of placing winning bets are extremely high in bank stocks, if you've got anything more than the patience of a gnat. What else is objectively cheap? Insurance stocks. I add insurance stocks for much the same reason as banks. It is easy to find insurance stocks selling below book value, at the lower end of valuations ratios going back 10 and 20 years. Here is a chart of EMC Insurance (NASDAQ:EMCI) going back 10 years. It shows the price-to-book ratio steadily falling over time.  There are plenty of good insurers for which I could draw similar charts. Many of the same criticisms leveled at banks apply to insurers. The profitability of these businesses is also at cyclical lows. As an investor, the cheap sectors I have highlighted are exactly the kinds of situations that ought to attract your attention...and capital. Nothing exciting needs to happen to make a good return. You just need to see a return to average -- a reversion to the mean. Eventually, these things work themselves out, and investors make lots of money when they do. At bottom, that's the basis of Dean's sage advice. |

No comments:

Post a Comment